US Population Health Management (PHM) Market Size 2026-2030

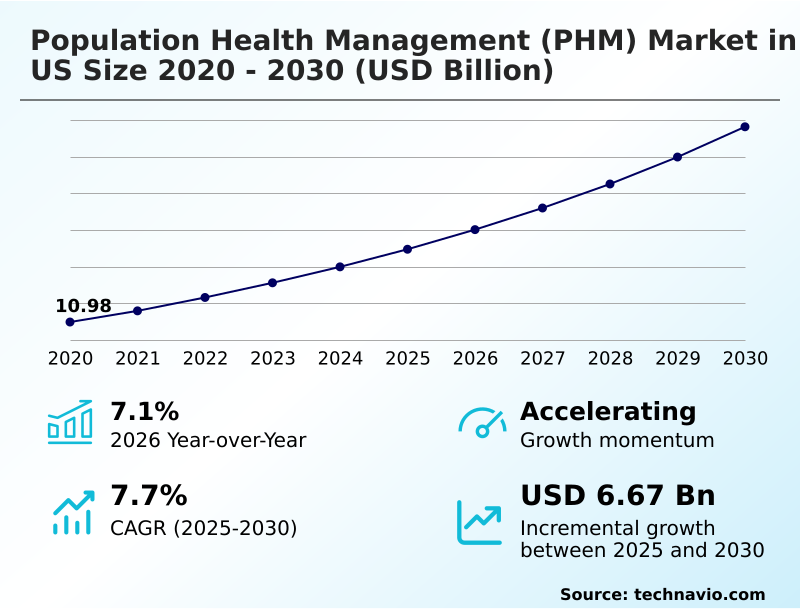

The us population health management (phm) market size is valued to increase by USD 6.67 billion, at a CAGR of 7.7% from 2025 to 2030. Transition toward value-based reimbursement frameworks will drive the us population health management (phm) market.

Major Market Trends & Insights

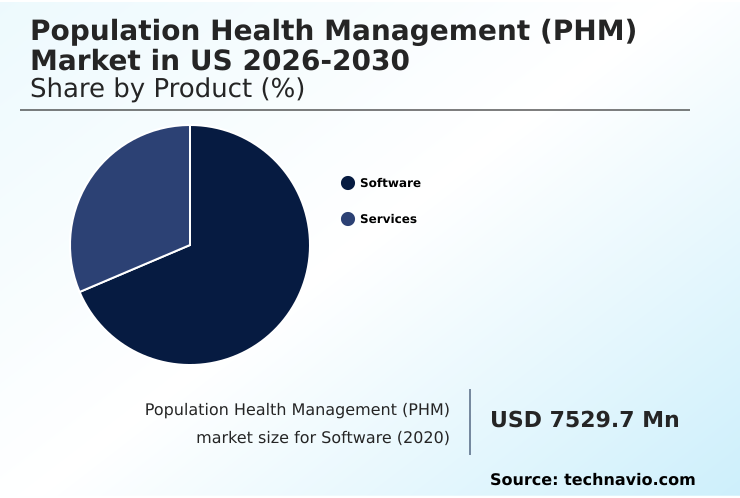

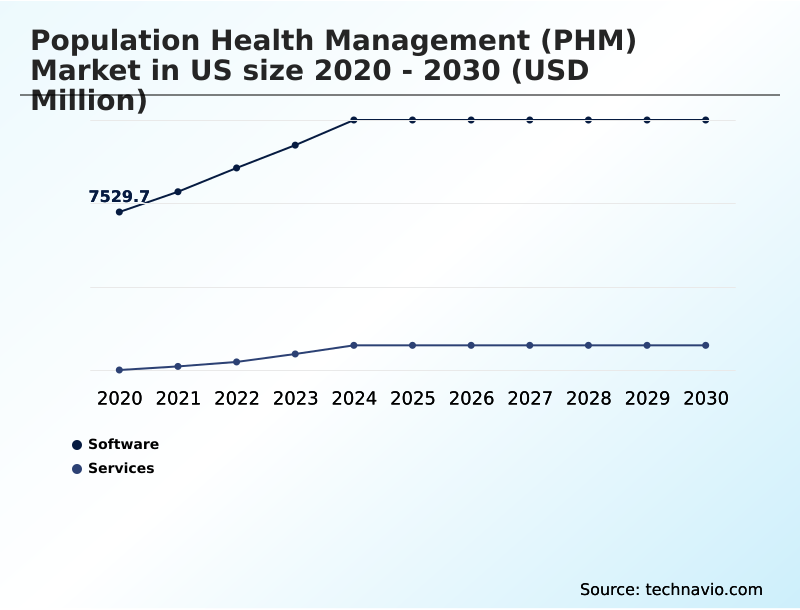

- By Product - Software segment was valued at USD 9.91 billion in 2024

- By Deployment - Cloud segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 10.65 billion

- Market Future Opportunities: USD 6.67 billion

- CAGR from 2025 to 2030 : 7.7%

Market Summary

- The population health management (phm) market in us is undergoing a significant transformation, driven by the imperative to improve population health outcomes while managing costs. This evolution is marked by a decisive shift towards proactive care models, where care management software and data aggregation platforms are crucial.

- Organizations are increasingly focused on patient cohort analysis and care gap identification to deliver targeted interventions. A key aspect is the use of a data aggregation platform for longitudinal patient records, which enables a more complete view of a patient's health journey.

- For instance, a health system can leverage predictive modeling algorithms to identify patients at high risk for hospital readmission, allowing for preemptive care coordination that enhances patient care and achieves operational efficiencies.

- However, the effectiveness of these strategies is contingent on overcoming challenges in healthcare data interoperability and ensuring robust patient data privacy, which remain critical focus areas for the industry as it moves deeper into value-based care.

What will be the Size of the US Population Health Management (PHM) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the US Population Health Management (PHM) Market Segmented?

The us population health management (phm) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Software

- Services

- Deployment

- Cloud

- On-premises

- End-user

- Healthcare providers

- Healthcare payers

- Employers and government bodies

- Geography

- North America

- US

- North America

By Product Insights

The software segment is estimated to witness significant growth during the forecast period.

The software segment in the population health management (phm) market in us is central to modern healthcare strategies. These digital tools serve as the backbone for shifting from reactive treatment to proactive prevention, emphasizing care delivery optimization.

Core functionalities include patient risk stratification and care gap identification, which are vital for value-based reimbursement models. Through electronic health record integration, these systems create a unified view, enabling healthcare analytics solutions to identify at-risk population management cohorts.

The integration of clinical decision support improves adherence to evidence-based care guidelines, with some providers reporting a 15% improvement in protocol compliance. This focus on data-driven intervention and population health outcomes is essential for managing chronic diseases effectively.

The Software segment was valued at USD 9.91 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic deployment of population health management solutions is pivotal for improving care for high-risk populations. Organizations are leveraging phm analytics for value-based contracts to align financial incentives with positive patient outcomes. A core focus involves phm strategies for chronic condition management, where data-driven interventions can significantly reduce long-term healthcare costs.

- The role of ai in patient risk stratification is expanding, enabling providers to identify vulnerable individuals with greater precision than methods used just a few years ago. Simultaneously, integrating sdoh into care management workflows is becoming standard practice, acknowledging that non-clinical factors are critical determinants of health.

- The success of these initiatives often hinges on optimizing patient engagement with phm tools, which requires intuitive interfaces and personalized communication. However, the industry continues to grapple with the challenges of data interoperability in phm, which can hinder the creation of a truly unified patient view.

- The debate over cloud vs on-premise phm deployment models continues, with organizations weighing security, scalability, and cost. Ultimately, measuring roi of phm technology investments remains a key priority for justifying expenditures and guiding future strategy.

What are the key market drivers leading to the rise in the adoption of US Population Health Management (PHM) Industry?

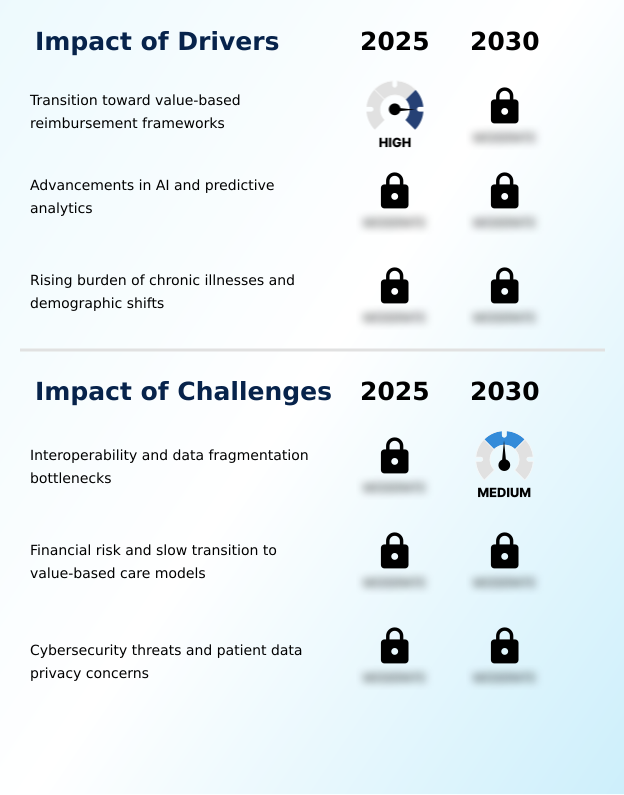

- The transition toward value-based reimbursement frameworks is the principal driver compelling healthcare organizations to adopt advanced population health management solutions.

- Market growth is propelled by fundamental shifts in the healthcare paradigm. The transition to value-based reimbursement frameworks makes population health outcomes a primary financial driver, pushing organizations toward proactive care models.

- Advancements in AI and predictive analytics are central to this, with some systems demonstrating a 30% increase in accuracy for at-risk population management. These technologies power everything from patient attribution logic to clinical workflow automation.

- The rising burden of chronic illnesses necessitates robust chronic disease management platforms, while demographic shifts heighten the need for efficient care delivery.

- Consequently, there is strong demand for healthcare analytics solutions that deliver actionable insights and support clinical quality improvement, making these tools indispensable for modern healthcare.

What are the market trends shaping the US Population Health Management (PHM) Industry?

- A key market trend is the strategic integration of social determinants of health into clinical workflows. This approach aims to create a more holistic and accurate view of patient well-being.

- Key market trends are reshaping care delivery through technological advancements. The systematic integration of social determinants of health into clinical workflows allows for a more comprehensive understanding of patient needs, with providers seeing an 18% improvement in identifying at-risk individuals.

- The shift toward decentralized care is powered by remote patient monitoring, which has been shown to reduce hospital readmissions by up to 25% for certain chronic conditions. Furthermore, there is an increasing focus on patient engagement tools and customized, quality measure reporting, enabling both patients and providers to track progress against health goals.

- These trends are underpinned by the growing adoption of telehealth integration and advanced health equity analytics to ensure equitable care distribution.

What challenges does the US Population Health Management (PHM) Industry face during its growth?

- Persistent interoperability issues and data fragmentation across disparate healthcare IT systems present a primary challenge that impedes the growth of the population health management market.

- The population health management market in us faces significant hurdles that temper its growth trajectory. The foremost challenge is healthcare data interoperability, with reports indicating that data integration issues can increase implementation project timelines by up to 40%. This data fragmentation, where information resides in siloed clinical data repository systems, severely hampers the effectiveness of value-based care analytics.

- Financial constraints also play a role, as the slow transition to value-based care models makes it difficult for some organizations to justify the investment in a new care coordination platform. Moreover, persistent cybersecurity threats and patient data privacy concerns require constant vigilance and investment, with security compliance accounting for nearly 15% of IT budgets for some providers.

Exclusive Technavio Analysis on Customer Landscape

The us population health management (phm) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the us population health management (phm) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of US Population Health Management (PHM) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, us population health management (phm) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Athenahealth Inc. - Offers a population health management platform integrating clinical and claims data to identify care gaps, coordinate care, and improve outcomes through network-enabled services.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Athenahealth Inc.

- Conifer Health Solutions LLC

- Cotiviti Inc.

- eClinicalWorks LLC

- Epic Systems Corp.

- Health Catalyst Inc.

- HealthEC LLC

- i2i Systems Inc.

- Innovaccer Inc.

- Koninklijke Philips NV

- Lightbeam Health Solutions

- McKesson Corp.

- Medecision Inc.

- Medical Information Tech Inc.

- Merative L.P.

- NextGen Healthcare

- Optum Inc.

- Oracle Corp.

- symplr Software LLC

- Tebra Technologies Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Us population health management (phm) market

- In September 2024, Oracle Corp. announced a strategic partnership with a major hospital network to deploy its cloud-native PHM platform, aiming to streamline care coordination for over two million patients.

- In November 2024, Epic Systems Corp. launched an advanced predictive analytics module for its electronic health record system, designed to improve patient risk stratification for chronic diseases.

- In February 2025, UnitedHealth Group's Optum division completed the acquisition of a leading healthcare analytics startup for approximately $500 million to enhance its population health intelligence capabilities.

- In May 2025, athenahealth Inc. received certification for its new interoperability framework, ensuring compliance with updated federal data exchange standards for health information exchanges.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled US Population Health Management (PHM) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 175 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.7% |

| Market growth 2026-2030 | USD 6674.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.1% |

| Key countries | US |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The population health management (phm) market in us is advancing beyond foundational data aggregation toward sophisticated population health intelligence. The emphasis is on proactive interventions through tools for preventive care outreach and patient cohort analysis.

- Core to this evolution is the seamless electronic health record integration with a care coordination platform, which has been shown to reduce administrative workloads by up to 30%. Vendors are embedding predictive modeling algorithms and clinical decision support directly into clinical workflow automation. This allows for real-time care gap identification and supports chronic disease management.

- Furthermore, the integration of social determinants of health data and claims data analysis is enabling more precise patient risk stratification and health equity analytics. This shift toward holistic data use is a strategic imperative, directly impacting how organizations budget for technology and align with compliance standards for quality measure reporting and value-based care.

What are the Key Data Covered in this US Population Health Management (PHM) Market Research and Growth Report?

-

What is the expected growth of the US Population Health Management (PHM) Market between 2026 and 2030?

-

USD 6.67 billion, at a CAGR of 7.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Software, and Services), Deployment (Cloud, and On-premises), End-user (Healthcare providers, Healthcare payers, and Employers and government bodies) and Geography (North America)

-

-

Which regions are analyzed in the report?

-

North America

-

-

What are the key growth drivers and market challenges?

-

Transition toward value-based reimbursement frameworks, Interoperability and data fragmentation bottlenecks

-

-

Who are the major players in the US Population Health Management (PHM) Market?

-

Athenahealth Inc., Conifer Health Solutions LLC, Cotiviti Inc., eClinicalWorks LLC, Epic Systems Corp., Health Catalyst Inc., HealthEC LLC, i2i Systems Inc., Innovaccer Inc., Koninklijke Philips NV, Lightbeam Health Solutions, McKesson Corp., Medecision Inc., Medical Information Tech Inc., Merative L.P., NextGen Healthcare, Optum Inc., Oracle Corp., symplr Software LLC and Tebra Technologies Inc.

-

Market Research Insights

- The dynamics of the population health management (phm) market in us are shaped by the transition to value-based care, demanding sophisticated technological support. Member engagement strategies are evolving, with platforms achieving up to a 25% increase in patient portal adoption through targeted outreach.

- Provider performance scorecards are now integral, with data showing that real-time feedback can improve adherence to clinical quality improvement protocols by 18%. Successful wellness program management now relies on data-driven insights, linking directly to healthcare cost reduction. The integration of telehealth integration within PHM platforms has streamlined care transition management, reducing post-discharge complications.

- These advancements underscore a market focused on quantifiable results and operational efficiency.

We can help! Our analysts can customize this us population health management (phm) market research report to meet your requirements.

RIA -

RIA -