Green Steel Market Size 2026-2030

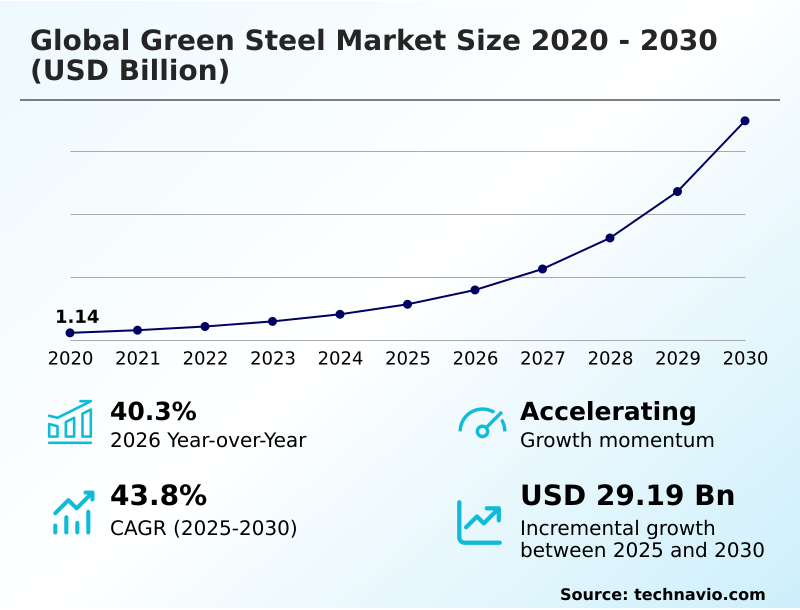

The green steel market size is valued to increase by USD 29.19 billion, at a CAGR of 43.8% from 2025 to 2030. Stringent environmental regulations and carbon pricing initiatives will drive the green steel market.

Major Market Trends & Insights

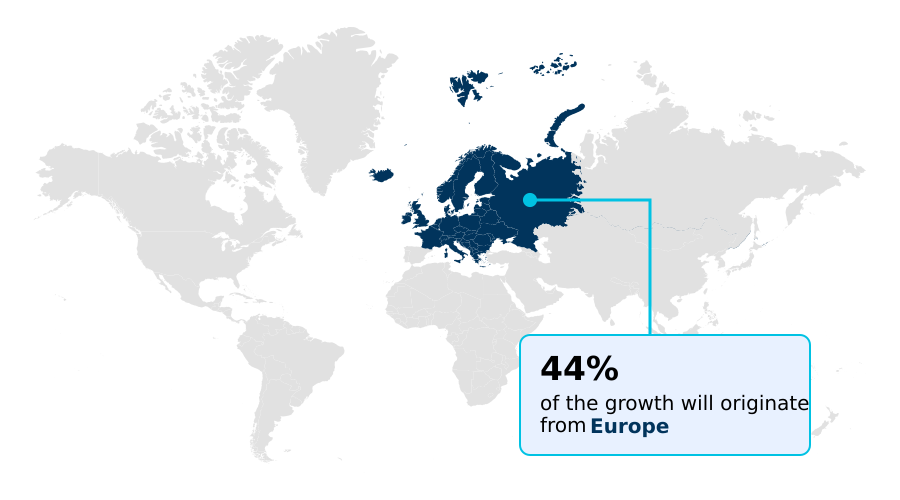

- Europe dominated the market and accounted for a 44.2% growth during the forecast period.

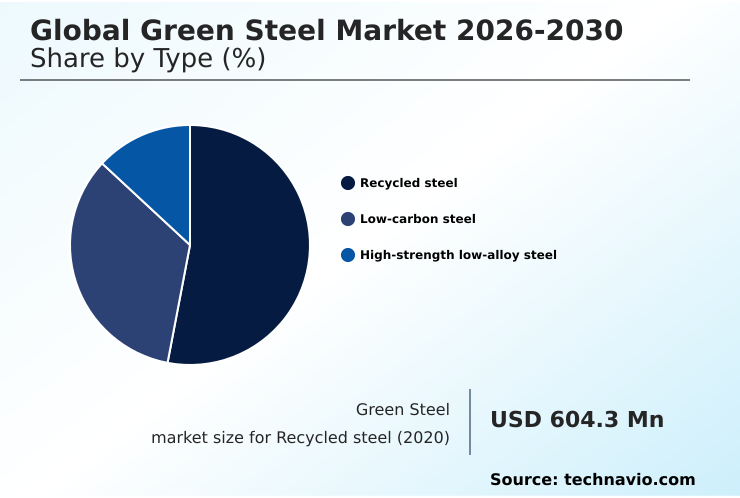

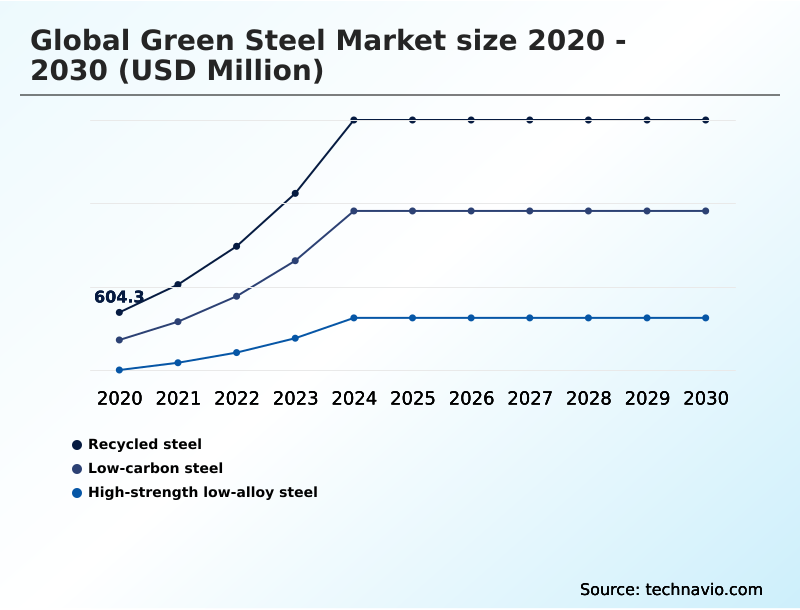

- By Type - Recycled steel segment was valued at USD 2.12 billion in 2024

- By Technology - Electric arc furnace segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 33.73 billion

- Market Future Opportunities: USD 29.19 billion

- CAGR from 2025 to 2030 : 43.8%

Market Summary

- The green steel market represents a fundamental shift in metallurgy, driven by the need to reconcile industrial production with environmental stewardship. This transition is propelled by stringent regulations and the implementation of frameworks like the carbon border adjustment mechanism, creating financial incentives to abandon carbon-intensive processes.

- Key trends include the adoption of hydrogen-based direct reduction and the expansion of electric arc furnace technology powered by renewables. Concurrently, corporate decarbonization targets from downstream sectors, particularly automotive, create strong demand-side pull for materials with a lower carbon footprint.

- However, the industry faces challenges related to the high capital costs of retrofitting plants and the nascent state of green hydrogen infrastructure. For example, a manufacturer aiming to reduce scope 3 emissions must secure a verifiable supply of low-carbon steel, a process that involves complex supply chain validation using technologies like blockchain to ensure traceability from production to final assembly.

- This move toward circular economy principles and sustainable sourcing is reshaping the entire value chain, making data transparency and material verification central to long-term business strategy and market positioning.

What will be the Size of the Green Steel Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Green Steel Market Segmented?

The green steel industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Recycled steel

- Low-carbon steel

- High-strength low-alloy steel

- Technology

- Electric arc furnace

- Hydrogen-based direct reduced iron

- Molten oxide electrolysis

- Others

- End-user

- Automotive

- Construction

- Industrial equipment and machinery

- Energy and power

- Others

- Geography

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- Turkey

- Rest of World (ROW)

- Europe

By Type Insights

The recycled steel segment is estimated to witness significant growth during the forecast period.

Market segmentation reflects diverse decarbonization pathways beyond primary routes. Technologies like the molten oxide electrolysis process and electrochemical metal extraction promise direct, carbon-free production.

For existing infrastructure, carbon capture utilization storage offers a transitional solution, while biomass-based reduction using bio-coke fuel replacement provides a lower-carbon alternative to coal. The development of advanced proton exchange membrane electrolyzer technology is critical for scaling green hydrogen.

This focus on sustainable material efficiency is vital for end-users, such as the industrial equipment decarbonization sector and for building renewable energy infrastructure steel.

Effective carbon footprint tracking, which can reduce embodied carbon in steel by over 80% compared to traditional methods, is essential for demonstrating compliance. All these approaches rely on access to carbon-free electricity sourcing for net-zero industrial manufacturing.

The Recycled steel segment was valued at USD 2.12 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 44.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Green Steel Market Demand is Rising in Europe Get Free Sample

The geographic landscape is shaped by regional strengths in technology and resources. Europe is pioneering low-carbon metallurgical innovation, focusing on hydrogen-based direct reduction and creating carbon-neutral industrial clusters.

The region's automotive industry is a key offtaker for advanced high-strength steel and other high-tensile strength alloys.

In APAC, the focus is on structural steel decarbonization through the expansion of electric arc furnace technology and electrified steelmaking processes, supported by policies promoting sustainable forestry for bio-coke. North America leverages its expertise in hydrogen injection in blast furnaces.

The ultimate goal across all regions is achieving zero-emission steel production, but progress is uneven. For example, regions with abundant renewables are advancing electrolytic iron production and other sustainable industrial materials 50% faster than those with carbon-intensive grids.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The transition to sustainable steel manufacturing hinges on several interconnected technological and economic factors. The hydrogen direct reduction ironmaking process stands as a primary pathway to decarbonization of heavy industry, though its viability depends on investment in hydrogen steel plants and reliable raw material sourcing for DRI.

- Simultaneously, electric arc furnace scrap recycling offers a circular route, but its effectiveness is tied to advanced technologies like robotic sorting for metal scrap. Innovations such as molten oxide electrolysis for steel and carbon capture in steel production provide alternative routes, though they face their own challenges in green steel adoption. For downstream users, the benefits are clear.

- High-strength low-alloy steel applications are crucial for designing next-generation products, particularly advanced steel for electric vehicles. To ensure authenticity, blockchain for steel supply chain and digital twins in steel manufacturing provide unprecedented transparency. The lifecycle assessment of steel products becomes a critical metric, especially for automakers focused on reducing scope 3 emissions in automotive.

- As demand grows, influenced by green building materials certification and circular economy for steel scrap principles, the entire value chain is being re-evaluated. For example, implementing renewable energy for EAF steelmaking can reduce operational energy costs by up to 20% compared to fossil-fuel-powered alternatives, a significant factor in supply chain planning.

- The impact of regulations like the carbon border adjustment impact further complicates international trade, making the shift to green hydrogen production for industry a strategic imperative.

What are the key market drivers leading to the rise in the adoption of Green Steel Industry?

- Stringent environmental regulations and carbon pricing initiatives are key drivers compelling the industry to adopt cleaner production technologies.

- Market expansion is propelled by a stringent industrial emissions framework, including the carbon border adjustment mechanism and emissions trading systems that incentivize low-carbon industrial processes.

- Downstream industries are accelerating their corporate decarbonization targets, increasing demand for materials that reduce scope 3 emissions and support green building certifications. This is particularly evident in the automotive sector's need for automotive lightweighting materials.

- Progress in renewable energy integration is critical, yet depends on ensuring renewable energy grid stability.

- The development of a resilient green hydrogen supply chain is equally vital, with advancements in lifecycle assessment data showing a potential 70% reduction in emissions for steel produced with green hydrogen compared to conventional methods.

- This supports the broader goal of sustainable urban development.

What are the market trends shaping the Green Steel Industry?

- A prominent trend is the development of integrated industrial clusters where steel manufacturing is co-located with large-scale hydrogen generation and renewable energy sites. This cross-sector synergy optimizes logistics and stabilizes clean energy supply.

- Key market trends center on enhancing efficiency and transparency. The development of industrial hydrogen hubs exemplifies cross-sector hydrogen synergies, optimizing logistics along dedicated carbon-neutral freight corridors. There is a strong focus on digital supply chain transparency, where blockchain supply chain traceability and digital twin production simulation provide verified environmental claims.

- These digital tools improve operational oversight by over 25% compared to legacy systems. Concurrently, an emphasis on circular economy principles is driving innovation in high-precision scrap beneficiation.

- The adoption of advanced scrap sorting technology, including robotic scrap sorting systems and chemical scrap purification techniques, is creating closed-loop recycling systems that produce higher-quality feedstock, with some processes improving scrap purity by 15%.

What challenges does the Green Steel Industry face during its growth?

- Substantial capital investment requirements and high operational costs present a key challenge affecting the industry's growth trajectory.

- The transition to fossil-free steel production is constrained by significant challenges. The substantial capital expenditure for retrofitting existing facilities into a modern industrial energy ecosystem remains a primary hurdle. Securing sustainable raw material procurement is another critical issue, with a scarcity of high-grade raw materials like direct-reduction grade iron ore and high-purity iron ore pellets.

- This elevates the need for iron ore beneficiation techniques. Furthermore, the operational cost of electrolysis for green hydrogen is still high, requiring advancements in high-capacity electrolyzers to become competitive with metallurgical coal alternatives.

- A reliable supply of direct reduced iron feedstock and high-purity scrap availability are essential, with supply chain disruptions causing production delays of up to 20% in some regions.

Exclusive Technavio Analysis on Customer Landscape

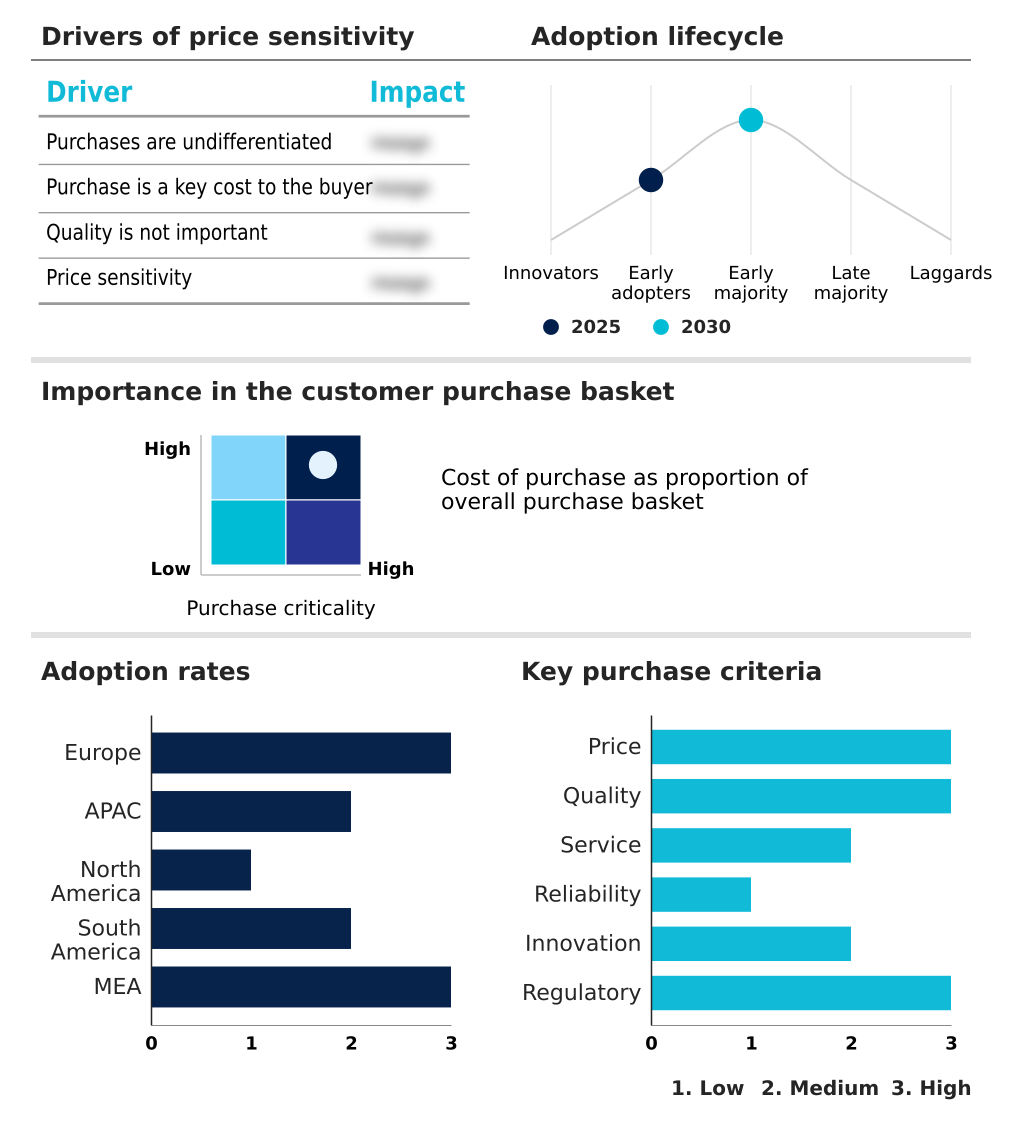

The green steel market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the green steel market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Green Steel Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, green steel market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ArcelorMittal S.A. - Offerings include recycled and renewably produced steel, alongside certified low-carbon steel solutions, addressing demand for sustainable materials across industrial applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ArcelorMittal S.A.

- BlueScope Steel Ltd.

- Boston Electrometallurgical Corp

- China BaoWu Steel Group Corp.

- Cleveland Cliffs Inc.

- Gerdau SA

- HBIS Group Co. Ltd.

- Hyundai Steel Co.

- JFE Holdings Inc.

- LIBERTY Steel Group

- Nippon Steel Corp.

- Nucor Corp.

- Outokumpu Oyj

- POSCO Co. Ltd.

- Salzgitter AG

- SSAB AB

- Tata Steel Ltd.

- thyssenkrupp Steel Europe AG

- United States Steel Corp.

- voestalpine AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Green steel market

- In February, 2025, a major North American utility provider initiated construction of a high-capacity hydrogen electrolyzer facility to create a localized energy ecosystem for heavy manufacturing plants in the Great Lakes region.

- In March, 2025, a leading European steel producer finalized a long-term agreement with a renewable energy consortium to procure wind-generated electricity for an upcoming electric arc furnace project, ensuring a stable supply of clean energy.

- In April, 2025, a prominent European regulatory agency implemented a revised framework for industrial emissions, mandating a 20% reduction in carbon intensity for all primary metal production facilities by 2030.

- In May, 2025, a prominent international recycling firm inaugurated an automated scrap processing center in the Port of Rotterdam, utilizing advanced sensory technology and AI to enhance raw material purity for green steel manufacturers.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Green Steel Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 314 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 43.8% |

| Market growth 2026-2030 | USD 29191.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 40.3% |

| Key countries | Sweden, Germany, UK, France, Italy, Spain, China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Brazil, Argentina, Colombia, Saudi Arabia, UAE, Turkey, Egypt and South Africa |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The industry is undergoing a pivotal transformation toward sustainable industrial materials, driven by a strict industrial emissions framework and the carbon border adjustment mechanism. This directly affects corporate decarbonization targets and scope 3 emissions reduction.

- At the core are two technology pathways: electric arc furnace technology, leveraging circular economy principles, and hydrogen-based direct reduction, requiring a robust green hydrogen infrastructure and access to direct-reduction grade iron ore. Boardroom decisions now focus on securing high-purity iron ore pellets and managing the high capital expenditure for retrofitting.

- Adopting digital twin production simulation, for instance, can reduce process energy use by over 12%. Innovations in high-precision scrap beneficiation, including robotic scrap sorting systems, are enhancing feedstock for advanced high-strength steel. Other methods like the molten oxide electrolysis process and biomass-based reduction offer alternative routes to fossil-free steel production, with technologies like proton exchange membrane electrolyzer becoming key.

- This evolution, verified via blockchain supply chain traceability and supporting green building certifications, is reshaping the industrial energy ecosystem.

What are the Key Data Covered in this Green Steel Market Research and Growth Report?

-

What is the expected growth of the Green Steel Market between 2026 and 2030?

-

USD 29.19 billion, at a CAGR of 43.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Recycled steel, Low-carbon steel, and High-strength low-alloy steel), Technology (Electric arc furnace, Hydrogen-based direct reduced iron, Molten oxide electrolysis, and Others), End-user (Automotive, Construction, Industrial equipment and machinery, Energy and power, and Others) and Geography (Europe, APAC, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

Europe, APAC, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Stringent environmental regulations and carbon pricing initiatives, Substantial capital investment requirements and high operational costs

-

-

Who are the major players in the Green Steel Market?

-

ArcelorMittal S.A., BlueScope Steel Ltd., Boston Electrometallurgical Corp, China BaoWu Steel Group Corp., Cleveland Cliffs Inc., Gerdau SA, HBIS Group Co. Ltd., Hyundai Steel Co., JFE Holdings Inc., LIBERTY Steel Group, Nippon Steel Corp., Nucor Corp., Outokumpu Oyj, POSCO Co. Ltd., Salzgitter AG, SSAB AB, Tata Steel Ltd., thyssenkrupp Steel Europe AG, United States Steel Corp. and voestalpine AG

-

Market Research Insights

- The market's dynamics are shaped by a confluence of regulatory pressures and supply chain innovations. The push for decarbonization is creating a notable green premium, with certified low-carbon materials commanding prices up to 30% higher than conventional steel. This shift compels manufacturers to focus on electrified steelmaking processes and direct reduced iron feedstock.

- Downstream, corporate buyers are driving demand for sustainable urban development and automotive lightweighting materials, with a focus on reducing embodied carbon in steel. Implementing digital supply chain transparency through blockchain can reduce verification costs by over 40% compared to manual audits.

- However, progress is tempered by infrastructure gaps in the green hydrogen supply chain and the scarcity of high-purity scrap availability. These challenges directly impact the operational cost of electrolysis and the capital expenditure for retrofitting, creating a complex strategic landscape for producers.

We can help! Our analysts can customize this green steel market research report to meet your requirements.

RIA -

RIA -