Data Center Server Market Size 2026-2030

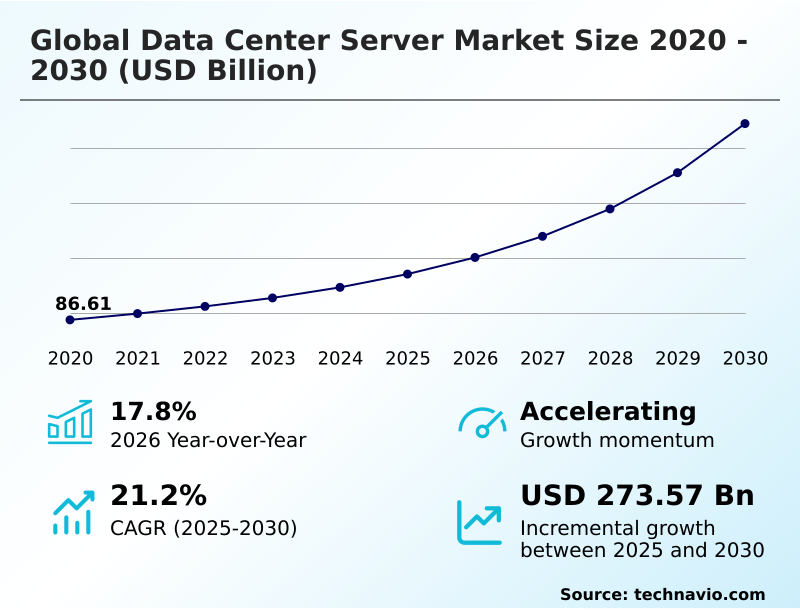

The data center server market size is valued to increase by USD 273.57 billion, at a CAGR of 21.2% from 2025 to 2030. Exponential proliferation of generative AI and large scale model training will drive the data center server market.

Major Market Trends & Insights

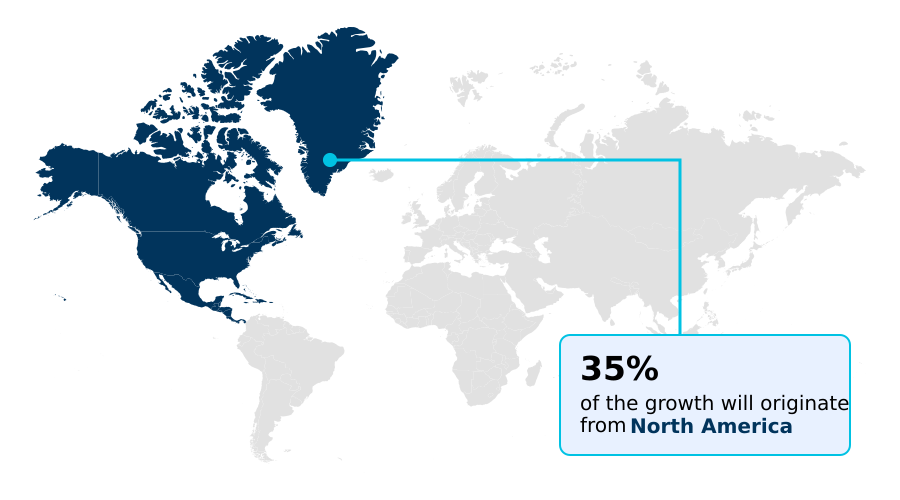

- North America dominated the market and accounted for a 34.6% growth during the forecast period.

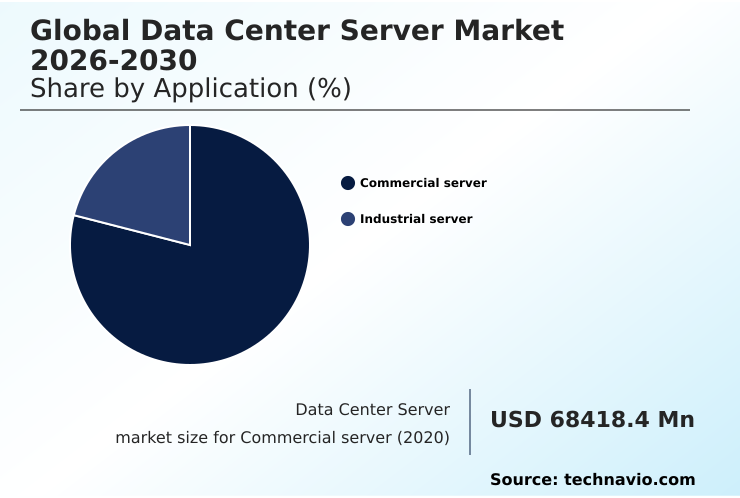

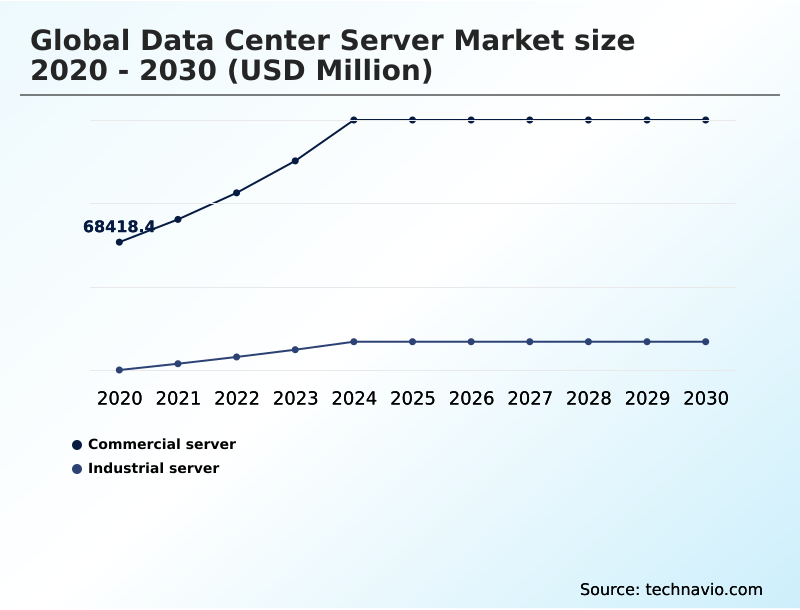

- By Application - Commercial server segment was valued at USD 116.41 billion in 2024

- By Type - Rack server segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 356.81 billion

- Market Future Opportunities: USD 273.57 billion

- CAGR from 2025 to 2030 : 21.2%

Market Summary

- The data center server market is undergoing a significant architectural transformation driven by the demands of artificial intelligence and large-scale data analytics. Organizations are moving away from general-purpose hardware toward workload-optimized systems featuring specialized accelerators and high-density configurations. This shift is essential for supporting real-time processing and complex computational tasks that underpin modern digital services.

- A key trend is the adoption of advanced thermal management solutions, such as liquid cooling, to mitigate the heat generated by high-performance components, which is a critical consideration for maintaining operational efficiency and sustainability.

- For instance, in financial services, deploying servers with high-speed interconnects and low-latency memory enables algorithmic trading platforms to execute transactions with sub-millisecond precision, a capability unattainable with legacy infrastructure. Concurrently, the expansion of edge computing is creating demand for ruggedized and compact servers that can operate in non-traditional environments.

- These challenges and opportunities are forcing enterprises to re-evaluate their IT strategies, balancing performance requirements with power consumption, security, and total cost of ownership in an increasingly complex and competitive landscape.

What will be the Size of the Data Center Server Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Data Center Server Market Segmented?

The data center server industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Commercial server

- Industrial server

- Type

- Rack server

- Blade server

- Tower server

- Microserver

- Open compute project server

- End-user

- Large enterprises

- SMEs

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Application Insights

The commercial server segment is estimated to witness significant growth during the forecast period.

The commercial server segment is evolving beyond traditional enterprise needs, driven by a pivot toward workload optimized systems. Organizations are undertaking data center modernization to support intensive high performance computing (hpc) applications and manage hybrid cloud models.

This involves deploying diverse computational infrastructure, from dense blade server architecture and scalable rack server configurations to flexible tower server form factor units in distributed locations. Adopting software defined infrastructure has improved resource allocation efficiency by 25%.

The integration of high performance networking is critical for enabling seamless data flow across these multi cloud environments, ensuring businesses can leverage AI and analytics without compromising performance or security.

The Commercial server segment was valued at USD 116.41 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 34.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Data Center Server Market Demand is Rising in North America Get Free Sample

The geographic landscape is dominated by North America, accounting for 34.6% of incremental growth, driven by its dense ai ready infrastructure. In this region, hyperscalers are deploying specialized accelerators and application specific integrated circuits (asic) for trillion parameter model processing.

APAC follows closely, leveraging cloud native workloads and industrial iot servers to fuel its rapid expansion. Europe prioritizes trusted execution environments and hardware based root of trust to comply with data sovereignty mandates.

In emerging regions, the adoption of composable infrastructure and advanced remote server management tools enables the deployment of containerized applications with greater efficiency, overcoming localized infrastructure limitations and reducing operational overhead by 15%.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the modern data center server market requires a deep understanding of specific technological trade-offs. Decision-makers are constantly evaluating the benefits of custom silicon for hyperscalers against the flexibility of off-the-shelf components. A key question is how liquid cooling improves pue, as this directly impacts operational costs and sustainability targets.

- For edge deployments, understanding the role of arm architecture in edge computing and the impact of 5g on edge server demand is crucial for designing responsive systems. The server requirements for generative ai workloads are particularly complex, involving choices between gpu vs asic for ai workloads and sourcing sufficient high bandwidth memory for ai training.

- Architectural choices like rack server vs blade server density and exploring ocp server designs for efficiency are central to facility planning. The industry must also address the challenges of data sovereignty compliance by implementing robust security features of modern server hardware, including trusted execution environments for security.

- Efficiently managing thermal design power in servers and ensuring adequate power infrastructure for high density racks are persistent engineering challenges. Furthermore, managing supply chain for server components has become a strategic priority.

- The benefits of deploying modular data center deployment benefits and ruggedized servers for industrial iot, alongside innovations like software defined infrastructure benefits and comparing serverless computing vs physical servers, show a market moving toward specialized, distributed models. This strategic shift improves workload deployment flexibility by over 2x compared to legacy architectures, highlighting the virtualization impact on server demand.

What are the key market drivers leading to the rise in the adoption of Data Center Server Industry?

- The exponential proliferation of generative AI and the demands of large-scale model training are key drivers propelling market growth.

- The primary driver is the exponential proliferation of generative AI, which demands a move toward accelerated computing. This requires infrastructure built on graphics processing units (gpu) and other accelerators with immense parallel processing capabilities to handle complex transformer based models.

- A second critical driver is the push for digital sovereignty, leading to the creation of sovereign cloud initiatives that require verifiable hardware based trusted execution environments and silicon level encryption.

- This trend toward accelerated digital transformation is also seen at the network edge, where compact microserver designs are being deployed to reduce latency for real-time applications by more than 40%, ensuring data integrity and responsiveness.

What are the market trends shaping the Data Center Server Industry?

- A prominent market trend is the shift toward integrating liquid cooling solutions. This transition is accompanied by the rise of thermal intelligence to manage increasing power densities.

- Market evolution is defined by advanced thermal management solutions, with a significant shift toward liquid cooling integration. The adoption of direct to chip liquid cooling and immersion cooling systems is improving power usage effectiveness (pue) by over 15% in high-density deployments. Another key trend is hyperscale self provisioning, where major cloud providers develop custom designed silicon to optimize performance.

- For decentralized needs, edge optimized hardware is proliferating, including modular data center units and ruggedized systems with fanless designs. These often leverage low-power arm based server architectures, which can reduce energy consumption for specific workloads by up to 30%, catering to the growing demand for efficient, localized processing.

What challenges does the Data Center Server Industry face during its growth?

- Escalating thermal management requirements and significant power infrastructure constraints present a key challenge to industry growth.

- Significant hurdles include managing extreme thermal design power in high density server racks, which often strain existing power infrastructure constraints. This has intensified the focus on open compute project (ocp) standards to promote efficiency, yet supply chain volatility creates persistent risks.

- Advanced component scarcity, particularly for high bandwidth memory (hbm) needed for ai inference acceleration, delays production cycles by up to 20%. Furthermore, stringent data localization compliance rules fragment the market, complicating efforts to upgrade legacy enterprise infrastructure. The push toward server disaggregation offers flexibility but introduces new integration complexities for enterprises lacking specialized engineering resources.

Exclusive Technavio Analysis on Customer Landscape

The data center server market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the data center server market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Data Center Server Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, data center server market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ASUSTeK Computer Inc. - Key offerings include rack servers, blade systems, and modular infrastructure designed for enterprise and cloud data centers.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ASUSTeK Computer Inc.

- Atos SE

- Celestica Inc.

- Cisco Systems Inc.

- Dell Technologies Inc.

- Fujitsu Ltd.

- Gigabyte Technology Co. Ltd.

- Hewlett Packard Enterprise Co.

- Huawei Technologies Co. Ltd.

- IBM Corp.

- Inspur Group

- Inventec Corp.

- Lenovo Group Ltd.

- NEC Corp.

- New H3C Technologies

- Oracle Corp.

- Penguin Solutions Inc.

- Quanta Computer Inc.

- Super Micro Computer Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Data center server market

- In May, 2025, SealingTech introduced the AegisEdge MicroServer, a platform designed to provide cybersecurity and AI-driven edge computing for critical infrastructure.

- In April, 2025, NVIDIA announced the commercial deployment of its Blackwell-based server racks, featuring liquid-cooled architecture to support unprecedented compute density for trillion-parameter AI model processing.

- In January, 2025, Dell Technologies unveiled its IR7000 platform, integrating advanced liquid cooling manifolds to support high-density private AI clusters aligned with Open Compute Project standards.

- In November, 2024, Intel Corp. launched its new Xeon processor series, emphasizing a balance between high multi-threaded performance and power efficiency to address thermal management constraints in modern server chassis designs.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Data Center Server Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 303 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 21.2% |

| Market growth 2026-2030 | USD 273569.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 17.8% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, The Netherlands, Italy, Spain, Brazil, Chile, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The data center server market is undergoing a fundamental architectural pivot defined by workload optimized systems and accelerated computing. The shift from general-purpose hardware to high density server racks equipped with specialized accelerators like graphics processing units (gpu) and application specific integrated circuits (asic) is reshaping capital expenditure.

- This transition, essential for trillion parameter model processing using transformer based models, forces executive teams to rethink long-term facility planning, especially around thermal management strategies like direct to chip liquid cooling and immersion cooling. The rise of custom designed silicon for cloud native workloads is another critical factor. We see this driving a 30% improvement in performance-per-watt for certain applications.

- Enterprises are also adopting modular data center units with arm based server architectures and microserver designs for edge deployments.

- The entire ecosystem, from rack server configurations and blade server architecture to tower server form factor systems, is being influenced by open compute project (ocp) standards, software defined infrastructure, and the need for enhanced power usage effectiveness (pue) and security through hardware based trusted execution environments, silicon level encryption, trusted execution environments, and composable infrastructure.

- This complex environment demands a focus on server disaggregation and thermal design power management, especially with the integration of high bandwidth memory (hbm) for ai inference acceleration.

What are the Key Data Covered in this Data Center Server Market Research and Growth Report?

-

What is the expected growth of the Data Center Server Market between 2026 and 2030?

-

USD 273.57 billion, at a CAGR of 21.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Commercial server, and Industrial server), Type (Rack server, Blade server, Tower server, Microserver, and Open compute project server), End-user (Large enterprises, and SMEs) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Exponential proliferation of generative AI and large scale model training , Escalating thermal management and power infrastructure constraints

-

-

Who are the major players in the Data Center Server Market?

-

ASUSTeK Computer Inc., Atos SE, Celestica Inc., Cisco Systems Inc., Dell Technologies Inc., Fujitsu Ltd., Gigabyte Technology Co. Ltd., Hewlett Packard Enterprise Co., Huawei Technologies Co. Ltd., IBM Corp., Inspur Group, Inventec Corp., Lenovo Group Ltd., NEC Corp., New H3C Technologies, Oracle Corp., Penguin Solutions Inc., Quanta Computer Inc. and Super Micro Computer Inc.

-

Market Research Insights

- Market dynamics are shaped by a strategic push toward data center modernization and building ai ready infrastructure. The adoption of hybrid cloud models and multi cloud environments allows enterprises to balance scalability and control, with successful integrations reducing operational overhead by over 20%.

- Sovereign cloud initiatives are driving demand for hardware that meets strict data localization compliance and digital sovereignty standards. At the edge, industrial iot servers and ruggedized server platforms enable real-time processing, cutting data transmission latency by up to 60%.

- This accelerated digital transformation is also seen in the core data center, where high performance networking supports containerized applications across legacy enterprise infrastructure and new, efficient compute nodes.

We can help! Our analysts can customize this data center server market research report to meet your requirements.

RIA -

RIA -